[ad_1]

The region’s commercial real estate market has boomed, but it’s not immune to mounting debt and rising interest rates

Ben Mandell is watching South Florida’s commercial real estate market, looking to break into a distressed asset as debt maturities approach amid high refinancing costs.

Ben Mandell is watching South Florida’s commercial real estate market, looking to break into a distressed asset as debt maturities approach amid high refinancing costs.

“It’s just part of the conversation these days in commercial real estate. Where is the distress? When will it strike? How can you take advantage of the opportunity?’ said Mandell, CEO of Miami-based Tricera Capital. “The writing is on the wall.”

South Florida boasts a reputation as a real estate haven, insulated from recession fears and rising foreclosures in markets like New York, Chicago and San Francisco. Even as the Federal Reserve is poised to continue rate hikes, the buzz in South Florida surrounds population and corporate growth and subsequent record rents across asset classes.

But the tri-county area won’t be unscathed by struggling commercial real estate sales, experts say.

Homeowners with maturing loans will face much more expensive refinances with higher interest rates than when they originally took out their debt. Not only will some owners fail to meet debt-to-service ratio requirements, they will find that banks are backing out of refinancing altogether, experts say.

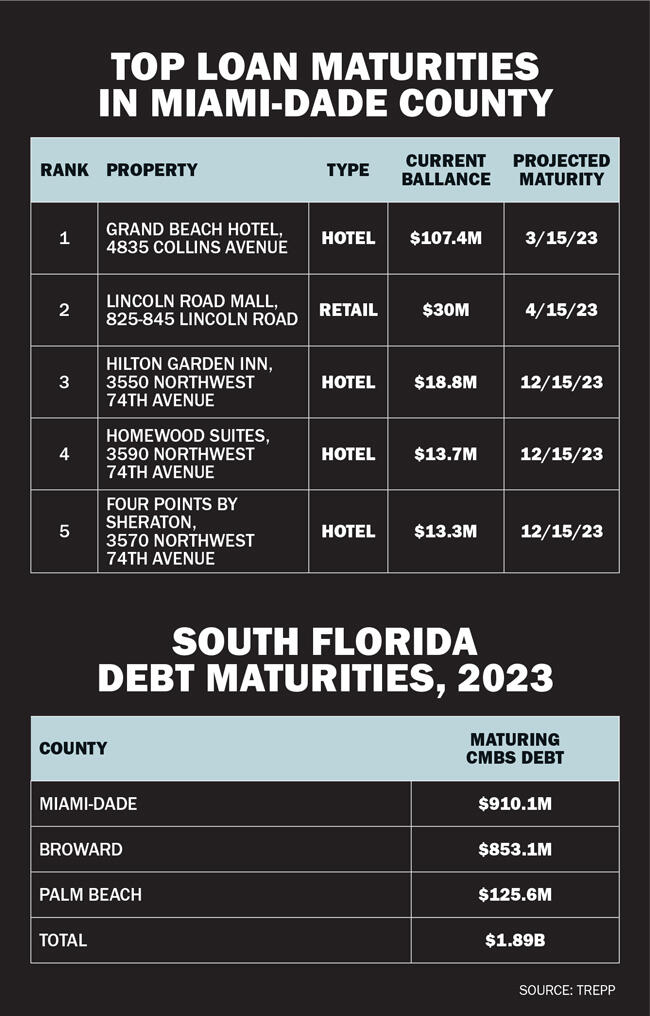

Across the tri-county area, nearly $1.9 billion in commercial mortgage-backed securities debt is maturing this year, according to Trepp. Miami-Dade County has the biggest chunk of that at $910.1 million. In Broward County, it’s $853.1 million and in Palm Beach County, the number is $125.6 million.

“South Florida has done much better and will continue to do so,” said Alex Horne, founder of Miami-based BridgeInvest. “It doesn’t mean it’s impervious to what’s going on in the market right now.”

The phone of embattled real estate investor David Gordon is buzzing. Calls are coming in from lenders who are in the process of foreclosing, have already foreclosed, or are simply afraid their borrowers won’t make upcoming due dates.

“We expect to be very busy this year,” said Gordon, managing director of Miami Beach-based ARC PE.

The company is betting on a $200 million venture buying spree nationwide this year, with 20% to 30% of that expected in South Florida.

“This is not going to be like 2008, where prices are going to drop 40 or 30 percent,” Gordon said. “There may be some small discounts. I think the number will be 5 to 20 percent across the board, including South Florida.”

Hospitality carries a large portion of the total amount of maturing debt.

Hospitality carries a large portion of the total amount of maturing debt.

The largest loan paid this year is $107.4 million on the 430-key beachfront Grand Beach Hotel at 49th Street and Collins Avenue in Miami Beach, according to Trepp. Property records show the owner is British billionaire Jacques Gaston “Tony” Murray, a 102-year-old World War II veteran who made his fortune in fire protection and air conditioning systems as well as real estate.

Three hotels west of Miami International Airport have a combined $45.8 million in debt. Boca Raton-based family-owned Economos Properties owns the Hilton Garden Inn, Four Points by Sheraton and Homewood Suites by Hilton at 3550, 3570 and 3590 Northwest 74th Avenue.

Back in Miami Beach, the retail property at 825-845 Lincoln Road has $30 million due this year, Trepp figures show. New York-based Jenel Real Estate owns the building.

It is unclear if plans are being made for these loans. The owners declined to comment.

A looming loan default and the prospect of a high-interest refinance or short-term bridge loan doesn’t necessarily spell doom. Landlords have options, said Mabelle Perez, who heads Berkadia’s hotel and hospitality division.

“It could be a combination of maybe a new partner coming in and saving the day, and maybe doing a loan workout with that lender before it gets to a short sale or foreclosure,” he said. “I think creativity will win.”

As a result, the extent of the pain South Florida property owners will experience is unknown, as is the potential volume of distressed asset deals.

Gordon isn’t exactly betting on a Brickell bonus, but on smaller assets, such as multifamily properties under $10 million, he said.

In a recent deal, ARC PE acquired a three-story mixed-use building in South Beach for $5 million, or 41 percent less than the seller’s purchase price a decade ago.

Although the foreclosure on the property, at 826 Collins Ave., did not stem from an inability to refinance — records show there is no outstanding loan on the property — the building’s features speak to how distress could arise. The retail and office spaces are vacant, and only the apartment building on the third level is leased.

Parts of Collins Avenue, including the area between Ninth and Fifth streets, have largely struggled as retailers have vacated space in recent years. And in other parts of South Florida, landlords haven’t benefited from increased demand for leases because they’ve been locked into non-renewing leases at much higher rents.

This may offer options for scavenger hunt investors this year.

For prices to come down, said Jalal “Jay” Shehadeh, EVP of US Century Bank in Doral, “it’s probably going to be in an area where occupancy is lower or where rents aren’t really going up.”

Even though the Fed began aggressively raising interest rates last spring, it hasn’t led to a big discount in commercial real estate prices in 2022. But the market’s reaction to the changing debt climate portends distress, experts say.

Investment sales fell as high financing costs prevented buyers from meeting sellers’ asking prices. At the very least, it showed that the South Florida market is not immune to rate hikes.

“I think that’s been building over the last year, and that’s been evidenced by the decline in sales volume,” said Shannon Rex of Colliers’ debt and equity finance group in South Florida.

“I think that’s been building over the last year, and that’s been evidenced by the decline in sales volume,” said Shannon Rex of Colliers’ debt and equity finance group in South Florida.

The office market was most affected. It had to beat last year’s second half with total sales of $776.9 million, down 70 percent year-on-year, according to Colliers data.

Office leasing has remained healthy, thanks to out-of-state financial and technology firms’ penchant for neighborhoods like Miami’s Brickell and Wynwood and downtown West Palm Beach. But lenders aren’t so enamored.

“Office is also the least desirable property to refinance, so there can be a lack of liquidity in the office sector,” said Rex.

In another indication of what’s to come, BridgeInvest saw an increase in inquiries this year for bridge loans. The company hears from borrowers who can’t secure refinancing from traditional lenders or don’t meet banks’ debt service coverage ratio requirements, according to Horn.

Industrial real estate is another market favorite. In the fourth quarter of last year, South Florida landlords were asking rents at $13.16 a square foot, up from $10.11 a square foot in the same period in 2021, even as vacancies fell slightly, according to Newmark.

However, BridgeInvest is working on a bridge loan for an industrial owner who found traditional financing options “closed,” Horn said. “No asset class is safe,” he said. “All agreements should sharpen their pencil.”

The influx of capital into South Florida will offset the angst expected elsewhere in the U.S., sources agreed. Tri-province skyrocketing rents across all property types will provide cash flow to offset high borrowing costs.

In Florida, we have other dynamics that keep valuations high relative to interest rates because you have companies moving here, in the migration,” Rex said. “I think Florida would be one of the last markets you would see” anguish.

However, others cautioned against counting high rents as a cushion.

“There are a lot of markets that I think are overvalued,” Gordon said. “Wynwood would be the biggest example of that.

“People are asking $150 per square foot [for retail],” he added. “I don’t see how, unless you’re an A-rated renter, you can afford those rents long-term, and there’s not enough foot traffic to really make sense. … Wynwood is one of the key areas where I believe there will be a drop in values.”

In this, Wynwood may just follow the path blazed by Miami Beach’s Lincoln Road, which has lost foot traffic and tenants in recent years to up-and-coming neighborhoods.

[ad_2]